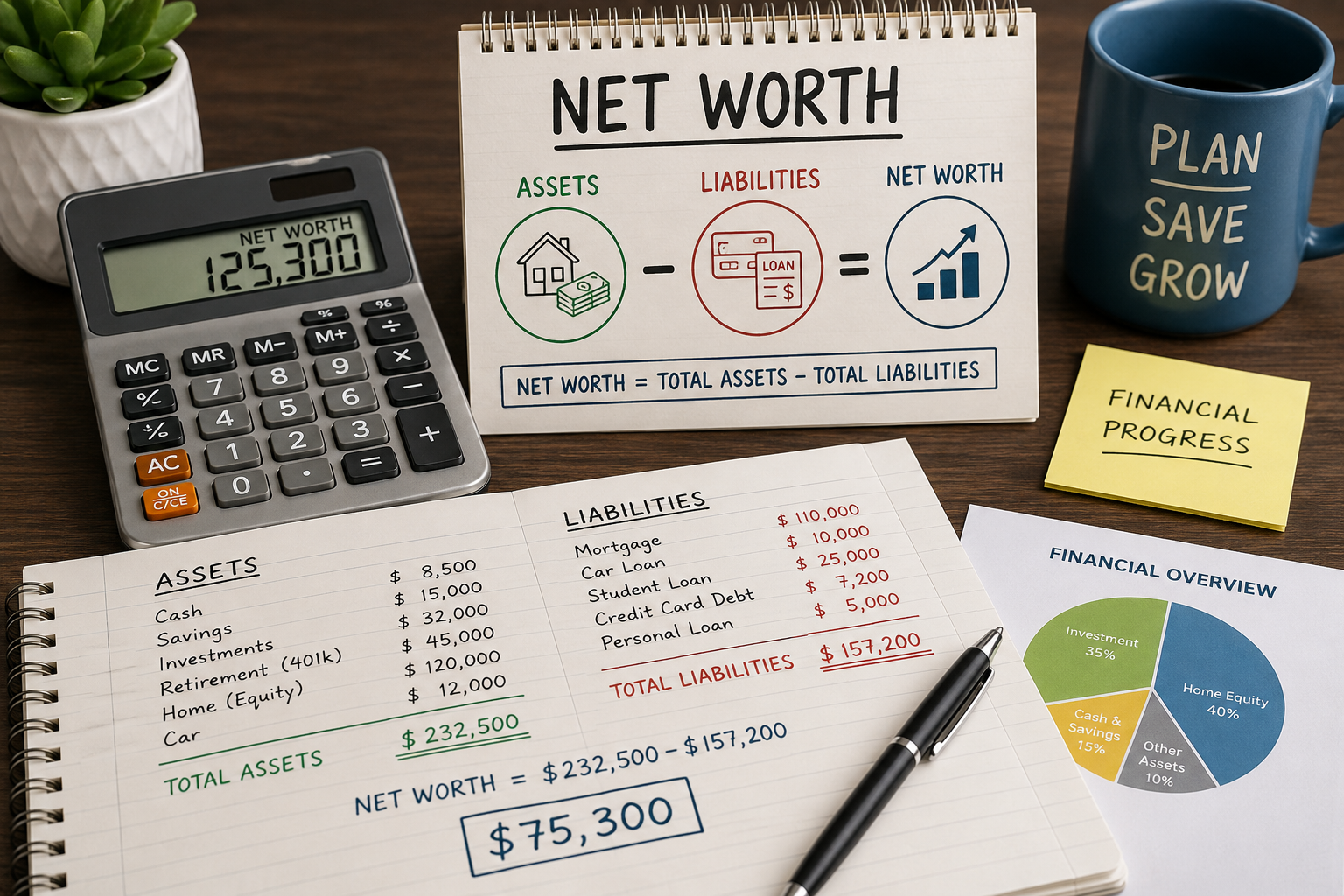

Net worth is calculated by subtracting total liabilities from total assets. The basic net worth formula is: net worth = total assets minus total liabilities. A person’s net worth can be positive or negative, and tracking it over time can show whether financial progress is improving, staying flat, or moving backward.

Introduction

Net worth is one of the simplest ways to measure financial progress. A budget shows what happens each month, but net worth shows the bigger picture. It combines what you own, what you owe, and how your overall financial position changes over time.

Many people search for how to calculate net worth because they want a clear number that summarizes their financial situation. The calculation is simple, but the details matter. You need to list assets accurately, list liabilities honestly, and update the numbers regularly.

This guide explains what net worth means, how to calculate your net worth, how the net worth formula works, how to use a net worth calculator, and how to create a basic net worth statement.

What Is Net Worth?

Net worth is the difference between the value of what you own and the amount you owe. In personal finance, net worth is often used to measure overall financial health because it combines assets and liabilities into one number.

If your assets are higher than your liabilities, your net worth is positive. If your liabilities are higher than your assets, your net worth is negative. A negative net worth does not mean a person has failed financially. It simply shows that debts are currently larger than assets.

Net worth meaning in simple terms

The net worth meaning is simple: net worth is what would remain if you sold your assets and paid off your debts. It is not the same as income. A person can have a high income and low net worth if spending and debt are high. A person can also have moderate income and strong net worth if assets grow and debts stay low.

Net Worth Formula

The standard net worth formula is straightforward:

Net worth = total assets – total liabilities

This formula can also be written as:

Total assets minus total liabilities = net worth

Net worth formula breakdown

| Formula Part | Meaning | Examples |

|---|---|---|

| Total assets | Everything you own that has financial value. | Cash, savings, investments, retirement accounts, home equity, vehicles. |

| Total liabilities | Everything you owe to lenders, creditors, or other parties. | Credit card debt, student loans, car loans, mortgage, personal loans. |

| Net worth | The difference between assets and liabilities. | Assets minus debts. |

Assets and Liabilities Meaning

Assets and liabilities are the two main parts of a net worth calculation. Assets increase net worth. Liabilities reduce net worth.

An asset is something you own that has value. A liability is a debt or financial obligation that you owe. The accuracy of your net worth calculation depends on listing both sides clearly.

Assets and liabilities compared

| Category | Meaning | Common Examples | Effect on Net Worth |

|---|---|---|---|

| Assets | Items, accounts, or property with financial value. | Checking account, savings account, investments, retirement account, home, car. | Increase net worth. |

| Liabilities | Debts or financial obligations owed to others. | Credit card balances, loans, mortgage, student loans, medical debt. | Decrease net worth. |

How to Calculate Net Worth

To calculate net worth, list all assets, add their values, list all liabilities, add their balances, and subtract total liabilities from total assets.

Step-by-step net worth calculation

- List your assets. Include cash, savings, investments, retirement accounts, real estate, vehicles, and other valuable property.

- Estimate the current value of each asset. Use realistic current values, not what you originally paid.

- Add total assets. This gives the total value of what you own.

- List your liabilities. Include credit cards, loans, mortgage balances, medical debt, and other obligations.

- Add total liabilities. This gives the total amount you owe.

- Subtract liabilities from assets. The result is your net worth.

The calculation should use current numbers. Old account balances or outdated home and vehicle estimates can make the result misleading.

Net Worth Calculation Example

A net worth calculation is easier to understand with an example. The table below shows a simple personal net worth example using assets and liabilities.

Example assets

| Asset | Estimated Value |

|---|---|

| Checking account | $2,000 |

| Savings account | $6,000 |

| Retirement account | $18,000 |

| Investment account | $5,000 |

| Vehicle value | $12,000 |

| Total assets | $43,000 |

Example liabilities

| Liability | Balance Owed |

|---|---|

| Credit card debt | $2,500 |

| Student loan | $9,000 |

| Car loan | $7,500 |

| Personal loan | $1,500 |

| Total liabilities | $20,500 |

Example net worth calculation

| Calculation Step | Amount |

|---|---|

| Total assets | $43,000 |

| Total liabilities | $20,500 |

| Net worth | $22,500 |

In this example, the person’s net worth is $22,500 because $43,000 in assets minus $20,500 in liabilities equals $22,500.

What Counts as an Asset?

An asset is anything you own that has financial value. For personal net worth, assets should be listed at realistic current value.

Common personal assets include:

- Checking account balances

- Savings account balances

- Emergency savings

- Certificates of deposit

- Investment accounts

- Retirement accounts

- Home value or home equity

- Vehicle value

- Business ownership value, if relevant

- Valuable personal property, if it can realistically be sold

Investment accounts can be part of personal assets, but beginners should understand how to invest in stocks and what market risks are involved before relying on stock investing to grow net worth.

Be careful with personal property estimates. Furniture, electronics, clothing, and collectibles may not be worth as much as expected. For a cleaner personal net worth statement, many people include only major assets with clear value.

What Counts as a Liability?

A liability is money you owe. Liabilities reduce net worth because they represent future payments or obligations.

Common personal liabilities include:

- Credit card balances

- Student loans

- Car loans

- Mortgage balance

- Personal loans

- Medical debt

- Buy now, pay later balances

- Tax debt

- Unpaid bills or collections

A full net worth calculation should include both large debts and smaller balances. Small debts can add up and make the overall picture less accurate if they are ignored.

If liabilities are difficult to organize or pay down, a structured debt management plan can help prioritize balances and improve net worth over time.

What Is a Net Worth Calculator?

A net worth calculator is a tool that adds assets, adds liabilities, and subtracts liabilities from assets. A calculator can make the process faster, but the result still depends on the numbers entered.

A net worth calculator is useful for beginners because it organizes the formula into categories. However, a spreadsheet, notebook, or simple table can also work.

A net worth calculator usually asks for:

- Cash and checking account balances

- Savings account balances

- Investment and retirement account values

- Real estate values

- Vehicle values

- Loan balances

- Credit card debt

- Other debts or liabilities

Net Worth Statement

A net worth statement is a simple document that lists assets, liabilities, and the final net worth number. It is like a personal financial snapshot.

A personal net worth statement can be updated monthly, quarterly, or yearly. Monthly updates are useful when paying down debt or building savings. Quarterly updates may be enough for people who do not want to track too often.

Simple net worth statement template

| Section | Item | Value or Balance |

|---|---|---|

| Asset | Checking account | $2,000 |

| Asset | Savings account | $6,000 |

| Asset | Retirement account | $18,000 |

| Asset | Investment account | $5,000 |

| Liability | Credit card debt | $2,500 |

| Liability | Student loan | $9,000 |

| Liability | Car loan | $7,500 |

| Final result | Net worth | $22,500 |

Personal Net Worth vs Income

Personal net worth and income are different. Income is money earned during a period of time. Net worth is the difference between assets and liabilities at one point in time.

A person with high income can still have low net worth if they spend most of their income or carry large debts. A person with lower income can build net worth over time by saving consistently, reducing debt, and investing carefully.

Income and net worth compared

| Measure | What It Shows | Example |

|---|---|---|

| Income | Money earned during a period of time. | Monthly salary, freelance income, business income. |

| Net worth | Assets minus liabilities at one point in time. | Savings, investments, property, and debts combined into one number. |

Both numbers matter. Income helps fund daily life and savings. Net worth shows whether financial progress is accumulating over time.

Positive Net Worth vs Negative Net Worth

A positive net worth means assets are higher than liabilities. A negative net worth means liabilities are higher than assets.

Negative net worth can happen for many reasons, including student loans, credit card debt, medical debt, car loans, or early career expenses. The goal is to improve the direction of net worth over time, not to feel discouraged by the first calculation.

How net worth can change

| Action | Effect on Assets | Effect on Liabilities | Effect on Net Worth |

|---|---|---|---|

| Saving money | Increases assets | No direct change | Increases net worth |

| Paying off debt | May reduce cash | Reduces liabilities | Usually improves net worth over time |

| Investing consistently | May increase assets over time | No direct change | Can increase net worth if investments grow |

| Taking on new debt | May or may not increase assets | Increases liabilities | Can reduce net worth |

How to Increase Net Worth

To increase net worth, focus on growing assets, reducing liabilities, or doing both at the same time. The best approach depends on the person’s current financial situation.

Practical ways to increase net worth

- Build emergency savings.

- Pay down high-interest debt.

- Contribute to retirement accounts when appropriate.

- Invest consistently for long-term goals.

- Reduce unnecessary monthly expenses.

- Avoid taking on debt for purchases that quickly lose value.

- Track net worth regularly.

- Increase income when possible.

- Use financial goals to stay focused.

Increasing net worth is not only about earning more. Spending habits, debt management, saving behavior, and investment decisions all affect long-term progress.

Long-term net worth can also grow when savings and investments have time to benefit from compound interest, especially when contributions stay consistent over many years.

How Often Should You Track Net Worth?

Net worth can be tracked monthly, quarterly, or yearly. The best frequency depends on the person’s goals and personality.

Monthly tracking can be useful when actively paying off debt, building savings, or trying to understand spending behavior. Quarterly tracking can reduce stress because investment values and account balances may move up and down from month to month.

Tracking frequency comparison

| Tracking Frequency | Best For | Main Benefit | Main Risk |

|---|---|---|---|

| Monthly | People paying debt or building savings actively. | Shows progress quickly. | Can feel stressful if values fluctuate. |

| Quarterly | People focused on steady long-term progress. | Balances detail and perspective. | Less immediate feedback. |

| Yearly | People who want a simple annual financial checkup. | Easy to maintain. | May miss problems for too long. |

Net worth tracking is more useful when it is connected to clear financial goals, such as saving more, reducing debt, or building long-term wealth.

Common Net Worth Mistakes

Net worth is useful, but it can be misleading if calculated carelessly. The goal is to create a realistic financial snapshot, not an inflated number.

Common mistakes include:

- Using unrealistic values for cars or personal items

- Forgetting small debts or unpaid balances

- Ignoring credit card balances

- Counting income as net worth

- Updating assets but not liabilities

- Comparing personal net worth to celebrities or public figures

- Checking too often and reacting emotionally

- Assuming home value is the same as home equity

Celebrity net worth numbers can be entertaining, but they are not useful benchmarks for personal finance. A personal net worth statement should focus on your own assets, your own liabilities, and your own progress over time.

Pepe The Toad’s Practical Note: Track Direction, Not Ego

Net worth tracking is most useful when it measures direction. The goal is not to use the number as a status symbol. The goal is to understand whether assets are growing, liabilities are shrinking, and financial decisions are improving the bigger picture.

A net worth number can move up or down for reasons outside your control, especially when investments or real estate values change. That is why the trend over time matters more than one monthly update.

The best approach is to connect net worth tracking to practical habits: budgeting, emergency savings, debt repayment, compound interest, and long-term financial goals.

Net Worth Checklist

- List all major assets.

- Use realistic current values.

- List all debts and liabilities.

- Include credit card balances.

- Use the formula: assets minus liabilities.

- Create a simple net worth statement.

- Update the calculation on a regular schedule.

- Track the trend over time.

- Use the result to guide savings, debt, and investment decisions.

Frequently Asked Questions

How do you calculate net worth?

To calculate net worth, add the value of all assets, add the balance of all liabilities, and subtract total liabilities from total assets. The formula is: net worth = total assets minus total liabilities.

How do I calculate my net worth?

To calculate your net worth, list your cash, savings, investments, retirement accounts, property, and other major assets. Then list credit card debt, loans, mortgage balances, and other liabilities. Subtract what you owe from what you own.

What is net worth?

Net worth is the difference between assets and liabilities. It shows what remains after subtracting debts from the value of everything owned. Net worth can be positive or negative depending on the balance between assets and debts.

What does net worth mean?

Net worth means the financial value left after subtracting liabilities from assets. It is a snapshot of financial position at one point in time and can be used to track financial progress over months or years.

What is the net worth formula?

The net worth formula is: net worth = total assets – total liabilities. This means you add everything you own, add everything you owe, and subtract debts from assets.

What is a net worth calculator?

A net worth calculator is a tool that helps add assets, add liabilities, and subtract liabilities from assets. It can be useful for beginners because it organizes the net worth calculation into clear categories.

What are assets and liabilities?

Assets are items, accounts, or property that have financial value. Liabilities are debts or financial obligations. Assets increase net worth, while liabilities reduce net worth.

What is a net worth statement?

A net worth statement is a document that lists assets, liabilities, and final net worth. It works like a personal financial snapshot and can be updated monthly, quarterly, or yearly.

How can I increase my net worth?

You can increase net worth by growing assets, reducing liabilities, or doing both. Common strategies include saving more, paying down debt, investing consistently, reducing unnecessary expenses, and tracking progress over time.

Should I include my car in net worth?

You can include a car in net worth if you use a realistic current resale value. If there is a car loan, include the vehicle value as an asset and the loan balance as a liability.

Conclusion

Net worth is one of the clearest ways to track financial progress. The calculation is simple: add assets, add liabilities, and subtract liabilities from assets. The result shows where your overall financial position stands at a specific point in time.

The real value of net worth tracking is not the first number. The value is the trend. When assets grow, debts shrink, and financial habits improve, net worth usually moves in the right direction over time.