Debt consolidation means combining multiple debts into one new payment, often through a debt consolidation loan, balance transfer, or repayment program. It may help organize credit card debt and simplify payments, but it does not erase debt. Consolidation works best when the new terms are better and spending habits change.

Introduction

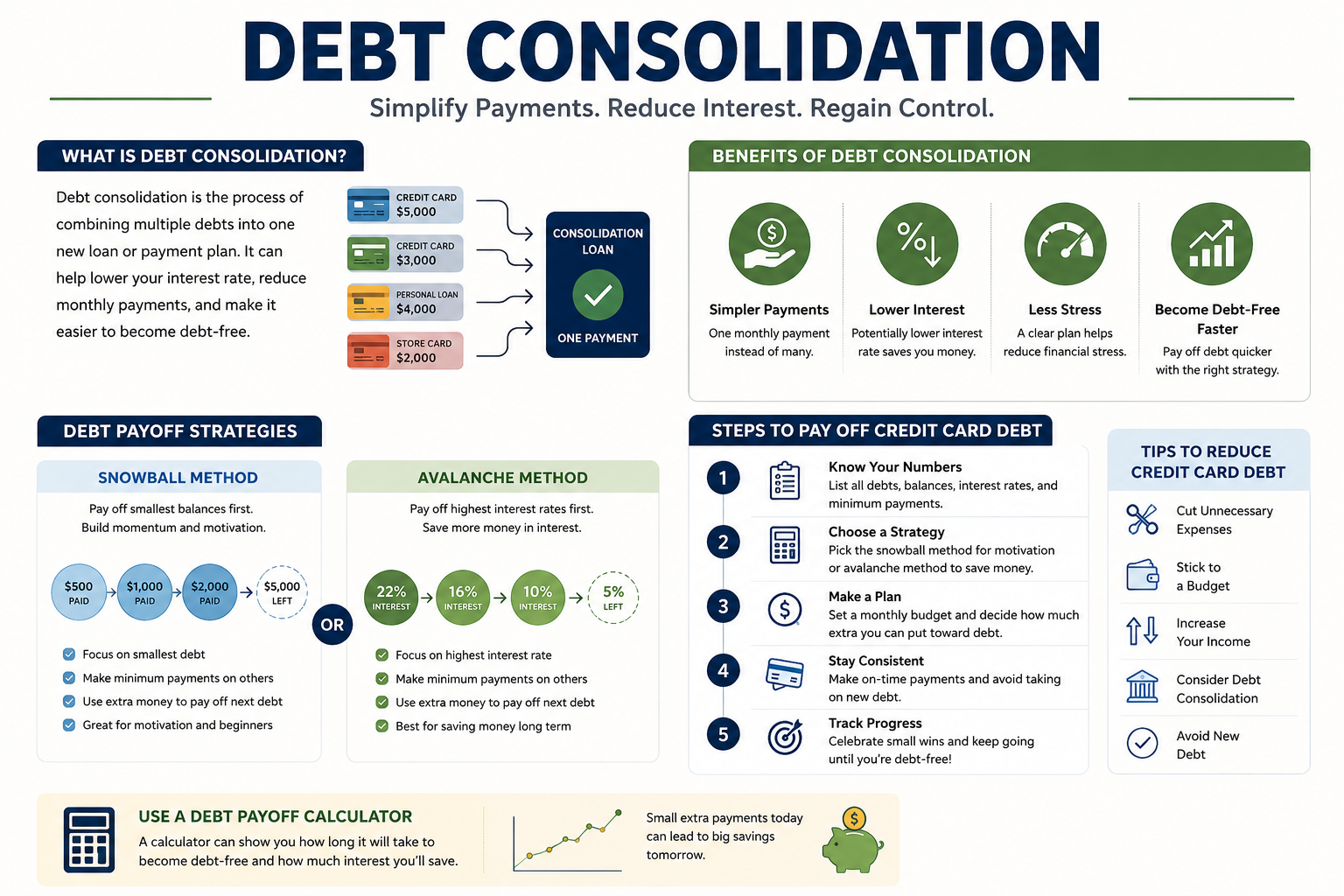

Debt consolidation is a common option for people who feel overwhelmed by multiple credit card balances, loan payments, interest rates, and due dates. Instead of managing several payments, the goal is to combine debts into one clearer repayment structure.

Many people search for debt consolidation because they want to know whether it can reduce stress, lower interest, simplify monthly payments, or help them get out of credit card debt faster. The answer depends on the interest rate, fees, repayment term, credit score, debt amount, and spending behavior.

This guide explains what debt consolidation is, how a debt consolidation loan works, how to consolidate credit card debt, when consolidation may help, when it may be risky, and how it compares with other debt payoff strategies.

What Is Debt Consolidation?

Debt consolidation is the process of combining multiple debts into one payment. Instead of paying several credit cards or loans separately, a person uses a new loan, balance transfer, or repayment program to organize the debt under one structure.

Debt consolidation does not automatically reduce the total amount owed. It changes how the debt is managed. In some cases, it may lower the interest rate or make payments easier to track. In other cases, it may extend the repayment period, add fees, or create more total cost over time.

Debt consolidation in simple terms

| Concept | Simple Meaning | Example |

|---|---|---|

| Debt consolidation | Combining multiple debts into one payment. | Using one loan to pay off several credit card balances. |

| Debt consolidation loan | A new loan used to pay off existing debts. | Borrowing $8,000 to pay off three credit cards. |

| Credit card debt | Money owed on one or more credit cards. | Balances carried month to month with interest. |

| Debt restructuring | Changing debt terms, payment structure, or repayment arrangement. | Working with a creditor or program to adjust payments. |

How Does a Debt Consolidation Loan Work?

A debt consolidation loan works by replacing multiple existing debts with one new loan. The borrower uses the new loan funds to pay off credit cards or other debts, then repays the new loan through one monthly payment.

The new loan may have a fixed interest rate, fixed repayment term, and predictable monthly payment. This can make repayment easier to manage. However, the benefit depends on whether the loan has better terms than the debts being consolidated.

Basic debt consolidation loan example

| Before Consolidation | Balance | Monthly Payment |

|---|---|---|

| Credit card 1 | $2,500 | $90 |

| Credit card 2 | $3,200 | $110 |

| Credit card 3 | $1,800 | $75 |

| Total | $7,500 | $275 |

| After Consolidation | Balance | Monthly Payment |

|---|---|---|

| Debt consolidation loan | $7,500 | $240 |

This example shows how consolidation can simplify payment structure. It does not prove that consolidation saves money. To know that, a person must compare interest rates, fees, repayment length, and total cost.

Debt Consolidation for Credit Card Debt

Debt consolidation is often used for credit card debt because credit cards can have high interest rates and multiple due dates. Consolidating credit card debt may make repayment easier if the new payment is affordable and the interest cost is lower.

The main risk is that the credit cards may become available again after consolidation. If a person consolidates credit card debt but keeps using the cards without a spending plan, total debt can become worse.

When credit card debt consolidation may help

- You have multiple credit card balances.

- You are missing due dates because there are too many payments to track.

- You qualify for a lower interest rate than your current cards.

- The new monthly payment fits your budget.

- You have stopped adding new credit card debt.

- You understand the fees and repayment term.

- You have a clear payoff plan after consolidation.

How to Consolidate Credit Card Debt

To consolidate credit card debt, first list all balances, interest rates, minimum payments, and due dates. Then compare consolidation options, estimate total cost, review fees, and decide whether consolidation improves the repayment plan.

Step-by-step credit card debt consolidation process

- List every credit card balance. Include the current balance, interest rate, minimum payment, and due date.

- Calculate total credit card debt. Add all balances to see the full amount owed.

- Review your monthly budget. Know how much you can realistically pay each month.

- Compare consolidation options. Look at personal loans, balance transfers, debt management programs, and other possible tools.

- Check fees and interest rates. A lower monthly payment is not always cheaper if fees or repayment length increase total cost.

- Choose a payoff strategy. Decide whether consolidation, avalanche, snowball, or another plan fits best.

- Stop adding new card debt. Consolidation can fail if the old cards are used again.

- Track progress monthly. Make sure the balance is actually going down.

Before choosing a consolidation option, a monthly budget template can help show whether the new payment actually fits your income, expenses, savings, and debt plan.

Common Debt Consolidation Options

There is more than one way to consolidate debt. The right option depends on credit score, income, debt amount, available offers, repayment discipline, and risk tolerance.

Debt consolidation options compared

| Option | How It Works | Possible Benefit | Main Risk |

|---|---|---|---|

| Personal debt consolidation loan | A loan is used to pay off several debts. | One fixed payment and possible lower interest rate. | Fees, higher cost, or new debt if cards are used again. |

| Balance transfer credit card | Credit card balances move to a new card, often with a promotional rate. | May reduce interest during the promotional period. | Transfer fees and higher rate after promotion ends. |

| Debt management plan | A credit counseling agency helps organize payments to creditors. | Structured repayment and possible creditor arrangements. | May require closing cards or following program rules. |

| Home equity loan or line of credit | Home equity is used to pay off unsecured debt. | May offer lower interest than credit cards. | Can put the home at risk if payments are missed. |

Debt Consolidation Loan vs Balance Transfer

A debt consolidation loan and a balance transfer both combine or move debt, but they work differently. A debt consolidation loan creates a new loan payment. A balance transfer moves credit card debt to another card.

Debt consolidation loan and balance transfer compared

| Feature | Debt Consolidation Loan | Balance Transfer |

|---|---|---|

| Payment type | Fixed loan payment. | Credit card payment. |

| Interest structure | Often fixed, depending on loan terms. | May start with a promotional rate. |

| Best for | People who want a predictable repayment schedule. | People who can repay during the promotional period. |

| Main risk | Longer term can increase total interest. | High rate may apply after promotion ends. |

| Behavior risk | Old credit cards may be used again. | New card may create more available credit to misuse. |

Debt Consolidation vs Debt Restructuring

Debt consolidation and debt restructuring are related, but they are not always the same. Debt consolidation usually combines debts into one new payment. Debt restructuring may involve changing the terms of existing debt.

Credit card debt restructuring can include changes to payment terms, hardship arrangements, settlement negotiations, or repayment programs. These options can have risks, fees, credit effects, or tax consequences depending on the situation.

Consolidation and restructuring compared

| Term | Basic Meaning | Typical Goal | Important Caution |

|---|---|---|---|

| Debt consolidation | Combining multiple debts into one payment. | Simplify payments and possibly lower interest. | Debt still must be repaid. |

| Debt restructuring | Changing debt terms or repayment arrangements. | Make debt more manageable. | May affect credit, fees, taxes, or creditor relationships. |

| Debt settlement | Trying to pay less than the full amount owed. | Reduce total payoff amount. | Can be risky and may damage credit if payments stop. |

What Is the Best Way to Pay Off Credit Card Debt?

The best way to pay off credit card debt depends on the balance amount, interest rates, income, credit score, budget, and behavior. Debt consolidation may help some people, but it is not always the best option.

For some people, the best approach may be a debt avalanche method, debt snowball method, debt management plan, or direct payoff plan without consolidation. The best strategy is the one that lowers risk, fits the budget, and actually reduces balances over time.

Credit card debt payoff options

| Strategy | How It Works | Best For |

|---|---|---|

| Debt consolidation | Combines debts into one payment. | People who qualify for better terms and need simpler repayment. |

| Debt avalanche method | Focuses extra payments on the highest-interest debt first. | People who want to reduce interest cost efficiently. |

| Debt snowball method | Focuses extra payments on the smallest balance first. | People who need motivation from faster small wins. |

| Debt management plan | Uses a structured repayment plan, often through credit counseling. | People who need help organizing payments. |

If consolidation is not the right fit, a structured debt management plan can still help organize balances, minimum payments, and payoff priorities.

Debt Avalanche Method and Debt Consolidation

The debt avalanche method focuses on paying the highest-interest debt first while making minimum payments on the rest. It can be useful when a person wants to reduce total interest cost.

Debt consolidation and the debt avalanche method can sometimes work together. For example, a person may consolidate some balances and still use the avalanche method for remaining debts. However, consolidation should not be used just to avoid looking at the real cause of the debt.

Debt avalanche method example

| Debt | Balance | Interest Rate | Payoff Priority |

|---|---|---|---|

| Credit card A | $3,000 | High | First |

| Credit card B | $1,200 | Medium | Second |

| Personal loan | $4,500 | Lower | Third |

How Credit Card Debt Calculators Can Help

A credit card debt calculator or credit card payoff calculator can help estimate how long repayment may take and how much interest may be paid under different payment amounts.

These tools are useful because they show the difference between minimum payments, extra payments, consolidation payments, and payoff strategies. The result is only an estimate, but it can make the repayment decision clearer.

A credit card payoff calculator usually asks for:

- Current balance

- Interest rate

- Minimum payment

- Extra monthly payment

- Target payoff date

- Possible consolidation loan terms

When Debt Consolidation May Help

Debt consolidation may help when it lowers the interest rate, simplifies repayment, creates a predictable payment schedule, and fits within the monthly budget.

It is usually more useful when the borrower has stopped adding new debt and is ready to follow a repayment plan. Consolidation is a tool, not a cure. It works only when the new structure supports real payoff progress.

Debt consolidation may be useful if:

- The new interest rate is lower than the current average rate.

- The new payment is affordable and realistic.

- The repayment term does not create unnecessary extra cost.

- Fees do not cancel out the benefit.

- You can avoid using paid-off credit cards for new spending.

- You have a monthly budget that supports the new payment.

- You understand the full loan agreement before accepting.

When Debt Consolidation May Be Risky

Debt consolidation may be risky when it creates a lower payment only by stretching debt over a much longer period. A lower monthly payment can feel helpful, but the total cost may increase if the loan lasts much longer.

Debt consolidation is also risky if it frees up credit cards and the borrower starts using them again. In that situation, the person may end up with the consolidation loan plus new credit card debt.

Debt consolidation warning signs

- The new loan has high fees.

- The interest rate is not lower than current debt.

- The monthly payment is still not affordable.

- The repayment term is much longer than expected.

- The lender or company uses pressure tactics.

- The plan requires stopping payments without understanding consequences.

- The old credit cards will likely be used again.

- The debt problem is caused by a budget gap that has not been fixed.

Debt Consolidation and Credit Scores

Debt consolidation can affect credit scores in different ways. Applying for new credit may create a hard inquiry. Opening a new loan can change account mix and average account age. Paying down credit card balances may help credit utilization if the cards are not used again.

The effect depends on the full credit profile and repayment behavior. Making payments on time is still important. Missing payments on a consolidation loan can damage credit and make the debt problem worse.

Possible credit effects

| Action | Possible Credit Effect | Why It Matters |

|---|---|---|

| Applying for a loan | May create a hard inquiry. | Can affect credit temporarily. |

| Paying down card balances | May improve credit utilization. | Lower card balances can support healthier credit usage. |

| Missing new loan payments | Can hurt credit. | Payment history is important for credit health. |

| Running cards up again | Can increase debt and utilization. | Creates new risk after consolidation. |

Paying down card balances may also affect your credit utilization ratio, especially if credit card balances become lower compared with available limits.

How to Decide if Debt Consolidation Is Worth It

Debt consolidation is worth considering only if it improves the repayment plan. A person should compare the current debt situation with the proposed consolidation option before making a decision.

Debt consolidation decision checklist

| Question | Why It Matters |

|---|---|

| Is the new interest rate lower? | A lower rate may reduce interest cost. |

| Are there fees? | Origination, transfer, or closing fees can reduce savings. |

| Is the payment affordable? | An unaffordable payment can lead to missed payments. |

| Is the repayment term longer? | A longer term may increase total interest. |

| Will the old cards stay unused? | Using them again can create more debt. |

| Does the plan fit the budget? | A debt plan fails if monthly cash flow cannot support it. |

Debt Consolidation Mistakes to Avoid

The biggest mistake is treating debt consolidation like debt elimination. The debt still exists. It has only been moved or reorganized.

Common mistakes include:

- Consolidating without comparing total cost.

- Choosing a lower payment without checking the longer repayment term.

- Ignoring fees.

- Using paid-off credit cards again.

- Consolidating debt without fixing the budget.

- Borrowing against a home without understanding the risk.

- Trusting companies that promise quick debt relief without explaining consequences.

- Missing payments on the new loan.

- Failing to track progress after consolidation.

Pepe The Toad’s Practical Note: Consolidation Is a Tool, Not a Reset Button

Debt consolidation can make debt easier to organize, but it does not erase the habits or cash flow problems that created the debt. If the monthly budget still does not work, consolidation may only move the problem into a new loan.

The best use of debt consolidation is strategic. Compare the old debt with the new offer, check the total cost, protect the monthly budget, and stop adding new balances.

A good consolidation plan should make debt simpler, cheaper, or more manageable. If it only creates a temporary feeling of relief, it may not solve the real problem.

Debt Consolidation Checklist

- You know the total amount of debt.

- You know the interest rate on each debt.

- You know the minimum payment on each debt.

- You have compared the new rate with current rates.

- You have checked fees and total repayment cost.

- You know whether the repayment term is longer.

- You know whether the monthly payment fits your budget.

- You have a plan to avoid new credit card debt.

- You understand the risks before signing.

- You will track progress after consolidation.

Frequently Asked Questions

What is debt consolidation?

Debt consolidation is the process of combining multiple debts into one payment. It is often used for credit card debt, personal loans, or other unsecured debts. It can simplify repayment, but it does not erase the debt.

What is a debt consolidation loan?

A debt consolidation loan is a new loan used to pay off existing debts. After the old debts are paid, the borrower repays the new loan through one monthly payment.

How do you consolidate credit card debt?

To consolidate credit card debt, list balances and interest rates, compare consolidation options, review fees and terms, choose a repayment method, pay off the old balances, and avoid adding new credit card debt.

Is debt consolidation good for credit card debt?

Debt consolidation may help with credit card debt if it lowers interest, creates an affordable payment, and supports a real payoff plan. It may not help if fees are high, the term is too long, or the cards are used again.

What is the best way to pay off credit card debt?

The best way to pay off credit card debt depends on interest rates, balances, income, and behavior. Options include debt consolidation, debt avalanche, debt snowball, debt management plans, and direct extra payments.

How can I clear credit card debt faster?

To clear credit card debt faster, reduce new charges, pay more than the minimum when possible, target high-interest balances, use a payoff plan, and consider consolidation only if it improves the total repayment picture.

What is the debt avalanche method?

The debt avalanche method is a payoff strategy that focuses extra payments on the debt with the highest interest rate first while making minimum payments on other debts.

What is a credit card debt calculator?

A credit card debt calculator estimates payoff time and interest cost based on balance, interest rate, and monthly payment. It can help compare minimum payments, extra payments, and consolidation options.

Can debt consolidation make debt worse?

Yes. Debt consolidation can make debt worse if the borrower uses old credit cards again, accepts high fees, takes a longer and more expensive repayment term, or misses payments on the new loan.

Is debt consolidation the same as debt settlement?

No. Debt consolidation combines debts into one payment. Debt settlement usually means trying to settle debt for less than the full balance. Debt settlement can have serious risks and may affect credit.

Conclusion

Debt consolidation can be useful for organizing credit card debt, reducing payment confusion, and possibly lowering interest cost. However, it is not a guaranteed solution. The debt still exists, and the new payment must fit the budget.

Before using a debt consolidation loan or another consolidation method, compare interest rates, fees, repayment terms, monthly payments, and total cost. A good debt consolidation plan should simplify repayment and support real progress, not create more room for new debt.